Contributed By:

Kushal Masand, IIFT Batch of 2012

The economic recession from which we are still recovering from, has brought with it a number of questions. Some of these questions will remain unanswered,not because we don’t have enough statistical data to prove it, but it will be impossible to expect economists from around the world to agree upon a single reason.

Moreover, in today’s complex economic world, there is only one thing on which economist can agree upon, and that is, a number of reasons joined force together to bring the recession of this level seen only during Great Depression. Some of these factors are sub-prime mortgage crisis, over-complicated financial instruments, bubble in commodity prices and real estate, unbalanced economic trade, easy credit conditions, regulations not able to keep pace with financial innovation, increased importance of shadow banking. These are some of the many reasons which contributed in recession.

One of the factors which lead to the economic recession has been the havoc the investment banking business, seen by many as risky,on to the commercial banking business, seen as traditional and not risky. To an idea how the securities played an important role in the recession can be understood by the fact that how mortgages were converted into AAA ranked debt securities under names as collateral debt obligation (CDO), Mortgage based securities (MBS), assets bases securities (ABS). But when another fact is added to this scenario that these securities were created not only from the good quality mortgages but also consisted of poor quality securities. By converting the mortgages to securities the banks havee removed the risk from their balance sheets and at the same time have created more liquidity to give more sub-prime mortgages, thus further increasing the risks for the people buying these securities. This all went well till the real estate prices were increasing and once the bubble burst all these securities turned into toxic assets which had to be pruned at the cost of tax-payers money.

Now let us see what were the changes brought by the Banking Act of 1933 popularly known as the Glass-Steagall Act.

Glass-Steagall act was introduced in 1933 by Senator Carter Glass and Congressman Henry Steagall. This act came after the Great Crash of 1929, during which one of every 5 American banks failed. Many people thought that the market speculation created by banks as the cause of this crash. This act was created to separate the investment banking business of the traditional commercial banks. It prohibited bank sales of securities and created Federal Deposit Insurance Corporation (FDIC), which insures deposits which guarantees the safety of deposits in member banks. In the early 1900’s, many commercial banks created there investment banking arms which corporate stock issues. This continued till great crash of 1929, after which a number f banks failed and the people confidence in US financial structure was low. To restore the public confidence, the Glass-Steagall Act was enacted. It prohibited the banks from using their own assets to invest in various securities. In 1920’s , a number of commercial banks were found guilty of misusing the depositors fund to acquire and trade into stocks and bonds.

So what Glass-Steagall act did was to strengthen the Federal Reserve. Member banks of Federal Reserve have to report all investment transactions and loans. Also it was mandatory for banks belonging to federal reserve to join FDIC and in order to join FDIC the had to be in sound financial position. Thus in the hindsight the act brought Darwin’s law of “ Survival of the fittest “ in the financial world of US banks where only the strong banks were able to survive. Thus by 1934, the failures of banks stopped and many banks reopened after joining the FDIC.

Now let us see how the Glass-Steagall Act was repealed layer by layer. The first effort started when some brokerage firms began encroaching in the banks territory by offering accounts that pay interest and offer credit and debit cards. Then in 1986, the Federal Reserve, under the pressure from Wall Street and intense lobbying, reinterpreted the section 20 of the Glass-Stegall Act, which bars commercial banks from engaging in the security business. It decided that banks can have 5 percent of their gross revenues from investment banking business.

Then in 1987, the fed board hears a proposal from the Citicorp, J.P. Morgan and Bankers Trust to allow banks to underwrite several securities like MBS and commercial paper. In the same year the Fed allows Chase Manhattan to underwrite the commercial paper. And at the same time it indicated that it may increase the limit that investment banking business can contribute in the gross revenues of the banks to the order of 10 percent.

In 1989, the Fed board approves the application from a number of banks to deal not only in commercial paper and municipal securities but also in debt and equity based securities.

In 1996, the Federal Reserve Board, under the Chairmanship of Alex Greenspan, a former director of J.P. Morgan, comes out with the rule that the investment banking business can contribute a hefty 25% to the gross revenues of the banks. Without considering that any bank holding company can remain under stipulated 25% norm.

Finally on 22nd October 1999, after 12 attempts iin 25 years, Congress repealed the Glass-Steagll Effect. A number of reasons were given to repeal the act. Some of them were that the investors are more knowledgeable today, and the existence of the sophisticated agencies, and the fact that banks of other countries doesn’t have to work under any regulations of such kind.

Now we come to question, had the Glass-Steagall Act had not been repealed, could we have saved ourselves from the economic downturn we are suffering from?

Some people say that it is most obvious to reinstate the Act, and the fact if it had not been repealed, the we couldn’t have seen the banks engaging themselves in so much of business relating to securities and creating toxic assets not only for themselves but also for the investors worldwide. And we didn’t had to save the so-called “ too big to fail “ banks which cost taxpayers their dearer money and could have been used to strengthen the public system, during the turnmoil.

Others advocate that the shadow banking system i.e. is nonblank lenders like Bear Stearns, Lehman Brothers, Goldman Sachs and Morgan Stanley sits at the epicenter of this turnmoil and that the fact these resides outside thee jurisdiction of Glass-Steagall Act. Also that banks like Washington Mutual, which collapsed even without the investment banking arm.

Economist can support either of the cause, but it is hard to remember any big banks which have failed during the time period of the Glass-Steagall Act. So it is to be decided by the conscience of the bankers and the tougher regulations from the governments that the world doesn’t have to suffer from a recession of such scale.

Sunday, August 29, 2010

Monday, August 23, 2010

Why Goldman Sachs made money & UBS lost during recession?

Contributed By: Shashank Kyatanavar

IIFT MBA (IB) 2010-12 Batch, Kolkata

The belief is investment banks more than any other institutions created the culture of excessive leverage, excessive risk and excessive bonuses that led to the downfall of the financial system, hence consequently should be the first ones to go under. But big daddy of investment banking, Goldman Sachs, debunking this theory earned a handsome profit & gave bonus; a bonus which infact is the largest bonus payouts in the company’s 140 year history.

On other hand we have one the safest destination where wealthiest people park their money , the Swiss Bank and the largest among them, Union Bank of Swizerland(UBS) suffering huge loss, an amount that is more than the sum needed to rescue Greece! Let’s try to understand this which seem to turn logic on its head.

Starting with UBS, it has lost about SwFr60 billion since the start of the credit crunch, partly because it was one of those deepest into the subprime, but also because it has fallen foul in a big way of the most countries tax authorities, especially US, who discovered by various means that the bank had been encouraging its residents to bank with it and engage in schemes which would avoid tax. This eventually led to a punitive settlement the fallout of which has been too much for a lot of clients and effect that they have took their business elsewhere. As a result the net money outflow for the division known as “Wealth management and Swiss Bank” was Swfr 33 billion, the division known as Wealth Management Americas lost Swfr12 billion and the Global Asset Management division had an outflow of Swfr11 billion

Goldman Sachs on other hand has reduced its overall leverage from a year ago with its fixed-income business, a less-risky arena than the illiquid derivatives and others products it loaded up on amid the credit bubble. It not only managed risk better, but it dramatically reduced is exposure to sub-prime mortgages. It also saw an opportunity in recession where it created a financial product that allowed one hedge fund, to bet against the value of housing. Also, the company has benefited because competitors like Lehman Brothers went bankrupt.

So is Goldman Sachs merely being punished for being a better bank than its peers? The answer is probably yes. And the reason for Goldman's profits - the source of the bonuses - are not from lending but from trading, using its own capital to buy stocks and bonds, and selling stocks and bonds short. And the reason Goldman Sachs thrived is just that it learned to play better than anyone else.

IIFT MBA (IB) 2010-12 Batch, Kolkata

The belief is investment banks more than any other institutions created the culture of excessive leverage, excessive risk and excessive bonuses that led to the downfall of the financial system, hence consequently should be the first ones to go under. But big daddy of investment banking, Goldman Sachs, debunking this theory earned a handsome profit & gave bonus; a bonus which infact is the largest bonus payouts in the company’s 140 year history.

On other hand we have one the safest destination where wealthiest people park their money , the Swiss Bank and the largest among them, Union Bank of Swizerland(UBS) suffering huge loss, an amount that is more than the sum needed to rescue Greece! Let’s try to understand this which seem to turn logic on its head.

Starting with UBS, it has lost about SwFr60 billion since the start of the credit crunch, partly because it was one of those deepest into the subprime, but also because it has fallen foul in a big way of the most countries tax authorities, especially US, who discovered by various means that the bank had been encouraging its residents to bank with it and engage in schemes which would avoid tax. This eventually led to a punitive settlement the fallout of which has been too much for a lot of clients and effect that they have took their business elsewhere. As a result the net money outflow for the division known as “Wealth management and Swiss Bank” was Swfr 33 billion, the division known as Wealth Management Americas lost Swfr12 billion and the Global Asset Management division had an outflow of Swfr11 billion

Goldman Sachs on other hand has reduced its overall leverage from a year ago with its fixed-income business, a less-risky arena than the illiquid derivatives and others products it loaded up on amid the credit bubble. It not only managed risk better, but it dramatically reduced is exposure to sub-prime mortgages. It also saw an opportunity in recession where it created a financial product that allowed one hedge fund, to bet against the value of housing. Also, the company has benefited because competitors like Lehman Brothers went bankrupt.

So is Goldman Sachs merely being punished for being a better bank than its peers? The answer is probably yes. And the reason for Goldman's profits - the source of the bonuses - are not from lending but from trading, using its own capital to buy stocks and bonds, and selling stocks and bonds short. And the reason Goldman Sachs thrived is just that it learned to play better than anyone else.

Sunday, August 15, 2010

Collapse Of Lehman Brothers | Story of brainy bankers in ideal market...

Harsimran Singh Sahni

Indian Institute of Foreign Trade

Kolkata Campus

Email- harsimransahni@gmail.com

The Collapse of Lehman Brothers

This was an economic 9/11!!

On September 15, 2008, Lehman Brothers filed for bankruptcy with $639 billion in assets and $619 billion in debt, Lehman's bankruptcy filing was the largest in history, surpassed Enron and WorldCom, which induced the financial crisis that swept through global financial markets in 2008.

The History of Lehman Brothers

Lehman Brothers, the largest investment bank, roots are traced back to a small general store founded by German immigrant Henry Lehman in Montgomery, Alabama, in 1844. In 1850, Henry Lehman and his brothers, Emanuel and Mayer, founded Lehman Brothers which was primarily involved in Investment Banking, equity and fixed income sales, research and trading. It was primary dealer in US Treasury securities market.

It has emerged stronger as it faced the plenty of challenges but it survived all- the railroad bankruptcies of 1800, the Great Depression of 1930s, Two World Wars. Despite its ability to survive the major challenges, it filed for the largest bankruptcy in US history on 15 September 2008.

Build-up to the Collapse

Mathematical Model for Money Making

From about 2001 and onwards, a credit bubble started to appear in the United States. Huge amount of capital moved into the country, in search of profit higher than the low rate of interest that existed at the time and at the same time, housing bubble was also in the making; and through the process of securitization the housing market was closely linked to the credit bubble in the U.S. financial system. The team of maths and physics PhDs showed, then CEO Dick Fuld, the calculations that how the bank will end up in profits if they invest in real markets and the next five years saw the bank borrowing billions of dollars to invest in housing market.

Lehman Brothers started giving insurance to the banks that have offered loans to customers and accepted that the chance of default on loans would be 5%. If 100 customers borrowing $1million have 5% assumed chance of default, given the interest rate @5%, the next year's $5 million would be worth 5/(5/100+1)=5/1.05=4.76 million now. So banks would have to pay minimum $4.76 million for insurance and to make money, Lehman Brothers would double the price to $9.5 million and expect to make $4.76 million out of each of these deals. And if more than ten of them default, the banks had to pay premium only for ten customers and the rest will be bear by Lehman Brothers. This type of deal is called Collateralised debt obligation contract in which the Lehman Brothers’ offering is senior tranche of CDO and one you are getting is junior tranche of CDO.

As it was unlikely to have more than ten borrowers defaulting, Lehman don’t have to pay anything and just pocketing the premium and it was considered as the safe investment as government deposits.

Pitfalls in Model

CDO is lot more risky than bank deposits, but Lehman Brothers didn’t realized them. The first source of error was that that they have assumed that each investor has 5% chance of default from historical data. There hasn't been a national drop of housing price since the great depression in the 1920s, so the chance that a borrower defaults was calculated on the basis of a good period when the housing prices surged. However, the housing market crashed in 2007 and to worsen this, 22% of these borrowers are sub-prime borrowers, those who had little income and had little hope of returning money which made lending quite risky.

The second source of error is that whether you make money from selling the CDO insurance for the bank depends on whether the borrowers return the money, which in turns depends on the economy. So if the economy goes down, you are a lot more likely to lose money. These two errors were sufficient to mask the risk in CDO.

Major cause of the Collapse- Subprime mortgage crisis

One novelty about housing bubble was that it involved the new group of economic actors: people who for the first time were able to buy house-subprime borrowers. In 2005 and 2006 Lehman was the largest producer of securities based on subprime mortgages.

The moment the market turned down, however, they would have to foreclose and securities based on this type of mortgage would register a loss. This is exactly what happened in August 2007 when the decline of US housing market started to register in major way in financial systems and major mortgage outfit went under and the amount of subprime mortgages was estimated at $2 trillion.

The indices came to play a crucial role in transforming a situation of economic loss in the housing market into a low level panic in the parts of financial system along with a lack of information about the location of the risks. However, it allowed investors to realize that the market was now lowering the price on securities based on subprime mortgages, they didn’t allowed the investors to figure out which securities were of low quality and which were not. The result was the fear about the hidden losses spread to all subprime mortgage-related bonds and CDO as well as to the institutions.

In 2007, due to the poor market conditions in mortgage space necessitated the substantial reduction in its resource and capacity and the firm closed its subprime lender, BNC Mortgage. As 2007 became 2008, during the months after the fall of Bear Stearns the general economic situation continued to worsen and value of many assets had fallen dramatically and the pressure shifted to another investment banks especially to Lehman. In 2nd fiscal quarter, Lehman reported losses of $2.8 billion and forced to sell $6 billion assets which further panic the investors, who feared that Lehman had quite a bit more of hidden losses.

Financial Market Fallout

The Lehman bankruptcy act as kind of detonator and set off the panic which ended up threatening not only US Financial system but also global financial system. Some of the institution owned Lehman bonds and were engaged in credit default swaps with Lehman which had direct effect of Lehman bankruptcy. But the indirect effects of Lehman bankruptcy were caused by the fear and rumours that now begin to circulate and were more dangerous than direct effects. This was the $613 billion bankruptcy, largest ever in US history. There were nearly eighty Lehman subsidiaries around the world that had close ties with US parent company which ensured that fallout of Lehman will immediately spread all over world.

Fig-1. Short Term and Long Term Trends of Global Economy

In Japan, the banks and insurance companies announced the losses $2.4 billion because of ties with Lehman. Similarly, Iceland’s financial institutions were very much hurt by spike in CDSs that followed Lehman’s fall. Fed and Treasury failed to realize that major actor Primary Fund, which held $785 million in Lehman bonds became worthless overnight which set off a run on money market. The existence of investments in Lehman bonds in one market firm made investors think that other money market firms might have Lehman bonds or hidden losses. The direct link to one actor, led to belief that all the actors in the market might have similar holdings having indirect effect. UBS AG suddenly lost $4 billion due to rumours whereas actual figure stood $300 million. (Fig-1)

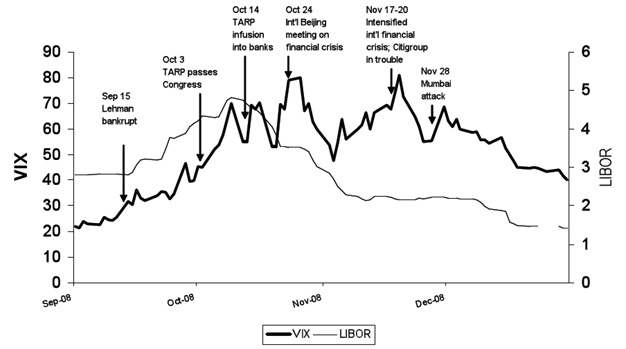

The process of financial disintegration that was set off by Lehman accelerated during the fall of 2008. The LIBOR-OIS spread peaked in mid October until decision was announced to invest TARP money directly into US banks and the fear Index shot up as well. (Fig-2)

Fig-2. Fear Index (VIX) and LIBOR during the Financial Crisis, August 2007 to September, 2009

The investors in various markets feared that some of the assets had suddenly become worth much less than they had thought and the loss of confidence that comes when they realized that there are hidden losses among their assets was the collapse of confidence. The second type of loss of confidence is related to action that investors and institutions take when they realized they no longer trust the proxy signs in the economy, it represented withdrawal of confidence.

Both types of confidence were part of event after Lehman bankruptcy which involved the fall of A.I.G and sudden demand by Bernanke for $700 billion to handle the crisis. Bernanke felt that if A.I.G went bankrupt this might break financial system and a decision to invest $80 billion in A.I.G. While the decision by the Fed to back A.I.G may have eliminated the breakdown in financial system, it also led to some confusion that why the FED had let Lehman fail? This was an economic 9/11!!

Indian Institute of Foreign Trade

Kolkata Campus

Email- harsimransahni@gmail.com

The Collapse of Lehman Brothers

This was an economic 9/11!!

On September 15, 2008, Lehman Brothers filed for bankruptcy with $639 billion in assets and $619 billion in debt, Lehman's bankruptcy filing was the largest in history, surpassed Enron and WorldCom, which induced the financial crisis that swept through global financial markets in 2008.

The History of Lehman Brothers

Lehman Brothers, the largest investment bank, roots are traced back to a small general store founded by German immigrant Henry Lehman in Montgomery, Alabama, in 1844. In 1850, Henry Lehman and his brothers, Emanuel and Mayer, founded Lehman Brothers which was primarily involved in Investment Banking, equity and fixed income sales, research and trading. It was primary dealer in US Treasury securities market.

It has emerged stronger as it faced the plenty of challenges but it survived all- the railroad bankruptcies of 1800, the Great Depression of 1930s, Two World Wars. Despite its ability to survive the major challenges, it filed for the largest bankruptcy in US history on 15 September 2008.

Build-up to the Collapse

Mathematical Model for Money Making

From about 2001 and onwards, a credit bubble started to appear in the United States. Huge amount of capital moved into the country, in search of profit higher than the low rate of interest that existed at the time and at the same time, housing bubble was also in the making; and through the process of securitization the housing market was closely linked to the credit bubble in the U.S. financial system. The team of maths and physics PhDs showed, then CEO Dick Fuld, the calculations that how the bank will end up in profits if they invest in real markets and the next five years saw the bank borrowing billions of dollars to invest in housing market.

Lehman Brothers started giving insurance to the banks that have offered loans to customers and accepted that the chance of default on loans would be 5%. If 100 customers borrowing $1million have 5% assumed chance of default, given the interest rate @5%, the next year's $5 million would be worth 5/(5/100+1)=5/1.05=4.76 million now. So banks would have to pay minimum $4.76 million for insurance and to make money, Lehman Brothers would double the price to $9.5 million and expect to make $4.76 million out of each of these deals. And if more than ten of them default, the banks had to pay premium only for ten customers and the rest will be bear by Lehman Brothers. This type of deal is called Collateralised debt obligation contract in which the Lehman Brothers’ offering is senior tranche of CDO and one you are getting is junior tranche of CDO.

As it was unlikely to have more than ten borrowers defaulting, Lehman don’t have to pay anything and just pocketing the premium and it was considered as the safe investment as government deposits.

Pitfalls in Model

CDO is lot more risky than bank deposits, but Lehman Brothers didn’t realized them. The first source of error was that that they have assumed that each investor has 5% chance of default from historical data. There hasn't been a national drop of housing price since the great depression in the 1920s, so the chance that a borrower defaults was calculated on the basis of a good period when the housing prices surged. However, the housing market crashed in 2007 and to worsen this, 22% of these borrowers are sub-prime borrowers, those who had little income and had little hope of returning money which made lending quite risky.

The second source of error is that whether you make money from selling the CDO insurance for the bank depends on whether the borrowers return the money, which in turns depends on the economy. So if the economy goes down, you are a lot more likely to lose money. These two errors were sufficient to mask the risk in CDO.

Major cause of the Collapse- Subprime mortgage crisis

One novelty about housing bubble was that it involved the new group of economic actors: people who for the first time were able to buy house-subprime borrowers. In 2005 and 2006 Lehman was the largest producer of securities based on subprime mortgages.

The moment the market turned down, however, they would have to foreclose and securities based on this type of mortgage would register a loss. This is exactly what happened in August 2007 when the decline of US housing market started to register in major way in financial systems and major mortgage outfit went under and the amount of subprime mortgages was estimated at $2 trillion.

The indices came to play a crucial role in transforming a situation of economic loss in the housing market into a low level panic in the parts of financial system along with a lack of information about the location of the risks. However, it allowed investors to realize that the market was now lowering the price on securities based on subprime mortgages, they didn’t allowed the investors to figure out which securities were of low quality and which were not. The result was the fear about the hidden losses spread to all subprime mortgage-related bonds and CDO as well as to the institutions.

In 2007, due to the poor market conditions in mortgage space necessitated the substantial reduction in its resource and capacity and the firm closed its subprime lender, BNC Mortgage. As 2007 became 2008, during the months after the fall of Bear Stearns the general economic situation continued to worsen and value of many assets had fallen dramatically and the pressure shifted to another investment banks especially to Lehman. In 2nd fiscal quarter, Lehman reported losses of $2.8 billion and forced to sell $6 billion assets which further panic the investors, who feared that Lehman had quite a bit more of hidden losses.

Financial Market Fallout

The Lehman bankruptcy act as kind of detonator and set off the panic which ended up threatening not only US Financial system but also global financial system. Some of the institution owned Lehman bonds and were engaged in credit default swaps with Lehman which had direct effect of Lehman bankruptcy. But the indirect effects of Lehman bankruptcy were caused by the fear and rumours that now begin to circulate and were more dangerous than direct effects. This was the $613 billion bankruptcy, largest ever in US history. There were nearly eighty Lehman subsidiaries around the world that had close ties with US parent company which ensured that fallout of Lehman will immediately spread all over world.

Fig-1. Short Term and Long Term Trends of Global Economy

In Japan, the banks and insurance companies announced the losses $2.4 billion because of ties with Lehman. Similarly, Iceland’s financial institutions were very much hurt by spike in CDSs that followed Lehman’s fall. Fed and Treasury failed to realize that major actor Primary Fund, which held $785 million in Lehman bonds became worthless overnight which set off a run on money market. The existence of investments in Lehman bonds in one market firm made investors think that other money market firms might have Lehman bonds or hidden losses. The direct link to one actor, led to belief that all the actors in the market might have similar holdings having indirect effect. UBS AG suddenly lost $4 billion due to rumours whereas actual figure stood $300 million. (Fig-1)

The process of financial disintegration that was set off by Lehman accelerated during the fall of 2008. The LIBOR-OIS spread peaked in mid October until decision was announced to invest TARP money directly into US banks and the fear Index shot up as well. (Fig-2)

Fig-2. Fear Index (VIX) and LIBOR during the Financial Crisis, August 2007 to September, 2009

The investors in various markets feared that some of the assets had suddenly become worth much less than they had thought and the loss of confidence that comes when they realized that there are hidden losses among their assets was the collapse of confidence. The second type of loss of confidence is related to action that investors and institutions take when they realized they no longer trust the proxy signs in the economy, it represented withdrawal of confidence.

Both types of confidence were part of event after Lehman bankruptcy which involved the fall of A.I.G and sudden demand by Bernanke for $700 billion to handle the crisis. Bernanke felt that if A.I.G went bankrupt this might break financial system and a decision to invest $80 billion in A.I.G. While the decision by the Fed to back A.I.G may have eliminated the breakdown in financial system, it also led to some confusion that why the FED had let Lehman fail? This was an economic 9/11!!

Friday, August 13, 2010

Outward FDI Philosophy: INDIA vs China

Outward FDI Philosophy: INDIA vs China

Outward Foreign Direct Investment (FDI) flows from developing countries especially from the large companies in China and India have of late generated significant international interest. As per the Boston Consulting Group (BCG) study, considering the top hundred companies from the developing world involved in outward FDI, more than sixty are from India and China. Predominantly, Foreign Direct Investments are made for acquiring assets outside the country. (Assets largely take the form of companies operating in developed and developing economies). A typical example is the acquisition of Corus (an English company) by Tata Steel, an Indian company. This is an outward FDI from India.

Traditionally, Indian companies have been into international acquisitions much longer than the Chinese companies and have steadily gained the tacit knowledge and intellect to deal with the complex management issues relating to managing international businesses. However, China in the last two decades has acquired several international assets with the help of its huge foreign currency reserves.

China and India's history and success of outward FDI

The outward FDI of the United States (US) for 2008 stood at $250 billion. Chinese, outward FDI during 2008 amounted close to $60 billion and that of India stood at $20 billion. Though the outward FDI of India and China are lower than the US, their growth has been significant. In recent years, the Chinese companies have become very aggressive; average overseas acquisition during the 1980 was around Rs. 4,500 crores per annum, equivalent of about half a billion US$, which climbed to an annual average of around Rs.12,000 crores during the 1990; Rs. 30,000 crores by 2004 and Rs.125,000 crores by the year 2007. In 2008 it amounted to Rs.200,000 crores.

In the last two years alone close to Rs.200,000 crores, or an equivalent of $40 billion, has been invested by Indian companies abroad; when we compare the same numbers with amount spent by Indian companies in domestic acquisitions, within India, it is less than Rs.50,000 crores, or one fourth the outward FDI figure. Over the last four years Tata Group alone has spent close to Rs.100,000 crores in various small sized and large global acquisitions. Other Indian groups like Aditya Birla, Essar and Bharti have all been very active in global acquisitions, as well. Companies like Jindal Steel and Godrej have also shown activity in term of overseas acquisition. Given the sheer size of such investments; outward FDI by India and China has grabbed the attention of the international community.

Differences in Underlying Philosophy

There is a fundamental difference in the underlying philosophy of the Chinese and the Indian companies with respect to outward FDI, and overseas acquisitions. When we say philosophy, we mean the objective for which the overseas acquisition is being pursued. The reason for such differences is attributed to the diverse political systems and the overall development strategies of the two countries, which is of late blurring.

Chinese Philosophy:

Large Chinese companies are run with the support from the government. There is strong interference of the Chinese government in the day-to-day operations and functioning of these companies. The Chinese government heavily influences the priority and rationing of the global investments by the Chinese companies and most of the outward FDI of China till 2004 has been towards energy security (the Chinese government wanted to secure its long term oil needs). Most Chinese state run oil companies have heavily invested in oil fields around the world, including in Africa and Russia. With foreign currency reserves in China close to US $2,000 billion, liquidity is abundant and is a major driver for the Chinese overseas acquisition; China's cumulative outward FDI is around US $150 billion. Comparatively, India's investment is in the range of US $70 to US $80 billion.

Till recently, China shied away from acquiring professionally run companies possessing strong brands, which has remained a forte of Indian acquisitions. Lack of international experiences and management talent and cultural and language barriers are being cited as reasons why Chinese companies have not been confident to manage geographically diversified operations, away from mainland China. If we analyze the key competencies of Chinese companies, it is their ability to manufacture low cost products for the developed world using their large-scale supply of semi skilled and cheap labor. China has been unable to put to use this key competence in their global acquisitions. Due to these shortcomings China has been unable to add value to its overseas acquisition of professionally managed global brands.

Chinese companies have failed in their acquisition attempts and inappropriately managed their global acquisitions; for example, failure by Chinalco to acquire the Australian mining company Rio Tinto and their failure in executing the North Rail Project in Philippines. But things have started to improve; and one can see a spurt of investments by Chinese companies in acquisition of well-run professional companies abroad. Although few, these include Lenovo's acquisition of IBM's 'think' personal computer business and Nanjing's acquisition of the British car maker MG Rover. Others include China's Bluestar acquisition of Belgium's Adisseo brand.

The sectoral investments too are getting diversified from the traditional energy related investments, with investments flowing into information technology, manufacturing, consumer durables, mining, internet, green technologies, agriculture and fisheries. Such a paradigm shift in the outward FDI philosophy is likely to position China in a competing stance with Indian corporates for attractive overseas assets, in the future.

Off late not only China, but other high growth developing economies like Brazil and South Africa too has shown significant level of outward FDI. These countries, together with India and China are controlling around 15 percent of the global Gross Domestic Product (GDP)

Indian Philosophy:

The outward FDI philosophy of India, contrarily, rests on very different fundamentals. Governmental interference in functioning of Indian corporate sector, for example is virtually non-existent. A large pool of Indian professionals having experience with multinationals and global corporations abroad, have over the last few years moved back to India due to its economic prosperity. They have been able to relate and deal with global corporations and understand management practices; and as a result many large and professionally run Indian companies have been successful in acquiring global and multinational companies.

Performing stock markets, good flow of foreign investments, a strong rupee, easy access to and availability of funds, both domestic and foreign currency, are resulting in fundamentally strong economic conditions in India. This gives an impetus to move forward with more outward FDI deals. Consistent and reasonably good corporate results have also left significant liquid cash, which is also a key driver for increased outward FDI. Further, the global economic crisis has provided attractive investment opportunities for the Indian companies; as a result India's global acquisitions have been much greater than their domestic acquisitions. In line with the Chinese outward FDI model, state owned Indian companies like Coal India, Oil and Natural Gas Corporation and Indian Oil Corporation have also created significant levels of outward FDI in securing energy assets. These companies are expected to pursue this more aggressively in the near future.

Indian companies have reached a stage of maturity in their management style and strategic planning for their operations. To that extent Indian acquisitions abroad have been founded on a strong fundamental synergy seeking behavior with their global acquisition targets. For example acquisition of Corus by Tata and Novelis by Hindalco are not knee jerk reactions; they have been well thought out acquisitions keeping in mind the strategic synergies that will arise.

Talking about Tata Steel's acquisition of Corus, Tata Steel had the worst productivity record during the 1990. In order to improve its competitiveness, it injected new technologies spending billions of dollars; and by the end of the 1990. Tata Steel became the world's most efficient steel maker. The company evolved a strategy to acquire global steel maker Corus, producing high value added steel having a capacity of around 20 million tonnes. Through this acquisition, Tata Steel not only enhanced its overnight steel making capacity multifold, but also secured sophisticated manufacturing technology, access to high value Western customers and achieved lower input costs. This is what we call strategic fit! On similar lines Tata Steel also acquired companies in other attractive markets like Singapore-based NatSteel and Millennium Steel in Thailand. The synergies proposed in this acquisition were very strategic and well thought out. The management expertise of the Tata Senior management and its advisors helped the company successfully conclude this acquisition.

A second example in this category is the acquisition of Novelis by Hindalco. What was the strategic fit in this acquisition? Hindalco being primarily an 'upstream' manufacturer of raw aluminum boasted of higher profitability in comparison to other aluminum manufacturers, but volatile sales price often pulled down its overall profitability. Hindalco wanted to become vertically integrated by getting into value added aluminum products in the form of sheets and foils, (known as 'downstream products'), primarily to stabilize its overall profitability. Profitability of the 'downstream' business is lower than 'upstream,' but is less volatile and also provides access to high value added customers, sophisticated manufacturing processes and access to technologies. Acquisition of Novelis provided this strategic fit to Hindalco. This is hailed as one of the most successful acquisitions in the Indian history.

Hence we can say that Indian companies have good strategies, founded on solid planned rationale; combined with effective managerial skills in successfully acquiring large global brands. Cultural and language compatibility has also helped the Indian acquisitions to be successful, especially in the task of post acquisition integration. The Chinese companies having failed in their acquisition attempts due to lack of the above knowledge, have pulled up their socks and have started to acquire professionally run Western companies and are high on the learning curve. Over time the philosophies of both the countries are likely to converge and pose stiff competition to each other and to the others in a growing global market.

Kumar Saurabh

2010-2012 Batch

IIFT, Kolkata

Indian Institute of Foreign Trade, Kolkata

By: Kumar Saurabh (2010-2012)

Outward Foreign Direct Investment (FDI) flows from developing countries especially from the large companies in China and India have of late generated significant international interest. As per the Boston Consulting Group (BCG) study, considering the top hundred companies from the developing world involved in outward FDI, more than sixty are from India and China. Predominantly, Foreign Direct Investments are made for acquiring assets outside the country. (Assets largely take the form of companies operating in developed and developing economies). A typical example is the acquisition of Corus (an English company) by Tata Steel, an Indian company. This is an outward FDI from India.

Traditionally, Indian companies have been into international acquisitions much longer than the Chinese companies and have steadily gained the tacit knowledge and intellect to deal with the complex management issues relating to managing international businesses. However, China in the last two decades has acquired several international assets with the help of its huge foreign currency reserves.

China and India's history and success of outward FDI

The outward FDI of the United States (US) for 2008 stood at $250 billion. Chinese, outward FDI during 2008 amounted close to $60 billion and that of India stood at $20 billion. Though the outward FDI of India and China are lower than the US, their growth has been significant. In recent years, the Chinese companies have become very aggressive; average overseas acquisition during the 1980 was around Rs. 4,500 crores per annum, equivalent of about half a billion US$, which climbed to an annual average of around Rs.12,000 crores during the 1990; Rs. 30,000 crores by 2004 and Rs.125,000 crores by the year 2007. In 2008 it amounted to Rs.200,000 crores.

In the last two years alone close to Rs.200,000 crores, or an equivalent of $40 billion, has been invested by Indian companies abroad; when we compare the same numbers with amount spent by Indian companies in domestic acquisitions, within India, it is less than Rs.50,000 crores, or one fourth the outward FDI figure. Over the last four years Tata Group alone has spent close to Rs.100,000 crores in various small sized and large global acquisitions. Other Indian groups like Aditya Birla, Essar and Bharti have all been very active in global acquisitions, as well. Companies like Jindal Steel and Godrej have also shown activity in term of overseas acquisition. Given the sheer size of such investments; outward FDI by India and China has grabbed the attention of the international community.

Differences in Underlying Philosophy

There is a fundamental difference in the underlying philosophy of the Chinese and the Indian companies with respect to outward FDI, and overseas acquisitions. When we say philosophy, we mean the objective for which the overseas acquisition is being pursued. The reason for such differences is attributed to the diverse political systems and the overall development strategies of the two countries, which is of late blurring.

Chinese Philosophy:

Large Chinese companies are run with the support from the government. There is strong interference of the Chinese government in the day-to-day operations and functioning of these companies. The Chinese government heavily influences the priority and rationing of the global investments by the Chinese companies and most of the outward FDI of China till 2004 has been towards energy security (the Chinese government wanted to secure its long term oil needs). Most Chinese state run oil companies have heavily invested in oil fields around the world, including in Africa and Russia. With foreign currency reserves in China close to US $2,000 billion, liquidity is abundant and is a major driver for the Chinese overseas acquisition; China's cumulative outward FDI is around US $150 billion. Comparatively, India's investment is in the range of US $70 to US $80 billion.

Till recently, China shied away from acquiring professionally run companies possessing strong brands, which has remained a forte of Indian acquisitions. Lack of international experiences and management talent and cultural and language barriers are being cited as reasons why Chinese companies have not been confident to manage geographically diversified operations, away from mainland China. If we analyze the key competencies of Chinese companies, it is their ability to manufacture low cost products for the developed world using their large-scale supply of semi skilled and cheap labor. China has been unable to put to use this key competence in their global acquisitions. Due to these shortcomings China has been unable to add value to its overseas acquisition of professionally managed global brands.

Chinese companies have failed in their acquisition attempts and inappropriately managed their global acquisitions; for example, failure by Chinalco to acquire the Australian mining company Rio Tinto and their failure in executing the North Rail Project in Philippines. But things have started to improve; and one can see a spurt of investments by Chinese companies in acquisition of well-run professional companies abroad. Although few, these include Lenovo's acquisition of IBM's 'think' personal computer business and Nanjing's acquisition of the British car maker MG Rover. Others include China's Bluestar acquisition of Belgium's Adisseo brand.

The sectoral investments too are getting diversified from the traditional energy related investments, with investments flowing into information technology, manufacturing, consumer durables, mining, internet, green technologies, agriculture and fisheries. Such a paradigm shift in the outward FDI philosophy is likely to position China in a competing stance with Indian corporates for attractive overseas assets, in the future.

Off late not only China, but other high growth developing economies like Brazil and South Africa too has shown significant level of outward FDI. These countries, together with India and China are controlling around 15 percent of the global Gross Domestic Product (GDP)

Indian Philosophy:

The outward FDI philosophy of India, contrarily, rests on very different fundamentals. Governmental interference in functioning of Indian corporate sector, for example is virtually non-existent. A large pool of Indian professionals having experience with multinationals and global corporations abroad, have over the last few years moved back to India due to its economic prosperity. They have been able to relate and deal with global corporations and understand management practices; and as a result many large and professionally run Indian companies have been successful in acquiring global and multinational companies.

Performing stock markets, good flow of foreign investments, a strong rupee, easy access to and availability of funds, both domestic and foreign currency, are resulting in fundamentally strong economic conditions in India. This gives an impetus to move forward with more outward FDI deals. Consistent and reasonably good corporate results have also left significant liquid cash, which is also a key driver for increased outward FDI. Further, the global economic crisis has provided attractive investment opportunities for the Indian companies; as a result India's global acquisitions have been much greater than their domestic acquisitions. In line with the Chinese outward FDI model, state owned Indian companies like Coal India, Oil and Natural Gas Corporation and Indian Oil Corporation have also created significant levels of outward FDI in securing energy assets. These companies are expected to pursue this more aggressively in the near future.

Indian companies have reached a stage of maturity in their management style and strategic planning for their operations. To that extent Indian acquisitions abroad have been founded on a strong fundamental synergy seeking behavior with their global acquisition targets. For example acquisition of Corus by Tata and Novelis by Hindalco are not knee jerk reactions; they have been well thought out acquisitions keeping in mind the strategic synergies that will arise.

Talking about Tata Steel's acquisition of Corus, Tata Steel had the worst productivity record during the 1990. In order to improve its competitiveness, it injected new technologies spending billions of dollars; and by the end of the 1990. Tata Steel became the world's most efficient steel maker. The company evolved a strategy to acquire global steel maker Corus, producing high value added steel having a capacity of around 20 million tonnes. Through this acquisition, Tata Steel not only enhanced its overnight steel making capacity multifold, but also secured sophisticated manufacturing technology, access to high value Western customers and achieved lower input costs. This is what we call strategic fit! On similar lines Tata Steel also acquired companies in other attractive markets like Singapore-based NatSteel and Millennium Steel in Thailand. The synergies proposed in this acquisition were very strategic and well thought out. The management expertise of the Tata Senior management and its advisors helped the company successfully conclude this acquisition.

A second example in this category is the acquisition of Novelis by Hindalco. What was the strategic fit in this acquisition? Hindalco being primarily an 'upstream' manufacturer of raw aluminum boasted of higher profitability in comparison to other aluminum manufacturers, but volatile sales price often pulled down its overall profitability. Hindalco wanted to become vertically integrated by getting into value added aluminum products in the form of sheets and foils, (known as 'downstream products'), primarily to stabilize its overall profitability. Profitability of the 'downstream' business is lower than 'upstream,' but is less volatile and also provides access to high value added customers, sophisticated manufacturing processes and access to technologies. Acquisition of Novelis provided this strategic fit to Hindalco. This is hailed as one of the most successful acquisitions in the Indian history.

Hence we can say that Indian companies have good strategies, founded on solid planned rationale; combined with effective managerial skills in successfully acquiring large global brands. Cultural and language compatibility has also helped the Indian acquisitions to be successful, especially in the task of post acquisition integration. The Chinese companies having failed in their acquisition attempts due to lack of the above knowledge, have pulled up their socks and have started to acquire professionally run Western companies and are high on the learning curve. Over time the philosophies of both the countries are likely to converge and pose stiff competition to each other and to the others in a growing global market.

Kumar Saurabh

2010-2012 Batch

IIFT, Kolkata

Indian Institute of Foreign Trade, Kolkata

Thursday, August 12, 2010

Subscribe to:

Posts (Atom)