And the year sailed by!!

It is really a great feeling to witness an entire year of articles and contributions vignette through the blog.

It has been a righteous forum for students as they wrote to share their thoughts, with freedom and zeal.

It has been 1 full year of activities lined up on the blog, And in some time from now, as the baton passes through to the new batch, let's hope that the blog scale newer heights.

Thanks to all for making this forum a great success!!

Happy Blogging!!

Wednesday, November 11, 2009

Thursday, September 17, 2009

The square rooted path to recovery

It has been almost a year since the Lehman collapsed and the world economy is still in its path to recovery. Speculations have been there about the path the recovery is going to take which is giving bulls the sleepless nights and economists are wary of predicting the new path the recovery is going to take. The recovery path charted out seems to be a square root shaped curve with every measure and indicator being back somewhat halfway of the normal level and then what seems to stay at a constant level for sometime. The global market capitalization fell from $75 trillion to $35 trillion post Lehman and market has now recovered $20 trillion of its value. In India sensex closed to 16454.45 after a fall from 21000, an increase in the excise collection over 22% for this month over the previous month and recovery of about $11 billion from the $12 billion capital outflows are a strong indicator that the economy is on its way back despite some hiccups but it is still a long way to say that it will bounce back to the previous levels. Emerging markets particularly the BRICs have returned to their pre Lehman levels but developed ones are still far below. These indicators support the fact about a slow recovery which still does not have the substance and the strength to take it upwards and to bring it back to the same level. For now the best way could be a pervasive action instead of waiting and watching economy bounce back and forth.

Contributed by:-

Divyank Gupta

Sunday, September 6, 2009

Money by Magic!!

In the wake of recession, Central Banks around the world are scrambling to increase money supply to boost spending and ease terms of credit. One way is through Borrowings: internal and external but they are weighed down by unwillingness and high terms of credit. Another instrument is Quantitative Easing which literally means reducing the monetary burden by creating more money.

Traditionally, Banks lower interest rates to stimulate economy but with interest rates inching to near zero levels, the method has limited application. Quantitative Easing is a policy where Central Banks purchase government and corporate bonds (issued by Banks), financial assets etc.

As the supply of bonds decrease it increases their price. Consequently, their utility as an attractive investment option shrinks or the yield on bonds diminishes. Hence, the Banks that sold the bonds are flush with excess money and they can lend the money to individuals or businesses as the yield on bonds is lower. This results in greater and easier access to credit and spurs economic activity.

Alternatively, for an economy unilaterally pursuing Quantitative Easing can be negative. For example, for US if too much money is created, it will lead to inflation or even hyperinflation. With rising inflation, investors will search for other financial instruments like gold or other currencies which could weaken dollar.

Quantitative Easing was first used by Central Bank of Japan to counter deflation. Lately, both US and UK have used it vigorously. The Bank of England has announced its intention to increase its exposure to £175 billion of which £125 billion has already been created. Central Banks across the world are taking proactive steps to negate recession, but will they it out to be a magic wand or a hex, can only be conjured.

Contributed By:

Ankit Agarwal

Playing the Weather Game

Today weather is not just an environmental issue – it is a major economic factor, more so if the economy is agriculture driven as is the case with India. It has an impact on corporate revenues and earnings of virtually every industry, including agriculture, energy, entertainment, construction, travel and many others. Until recently, there were very few financial instruments which could help companies in hedging against weather risks. However, since the inception of the weather derivative, things have changed.

In contrast to insurance, weather derivatives cover low risks and high probability events as per certain customised policies. Currently, energy companies and energy-related businesses use Weather Futures. However, there have been growing concerns and signs of potential growth in weather futures trading among agricultural firms and companies involved in tourism and travel as well. As such, India also has witnessed a welcome response to weather derivatives owing to the fluctuations in weather conditions. In India, Rainfall insurance has wide spread implications because despite the technological advancements, India has to depend on monsoon rains, with lack of irrigation. Still, it has been most often used in the U.S. and the U.K.

No doubt, this form of derivative trading is highly applicable in context with the present scenario but this carries along with it certain disadvantages as well for the daily models on the flip side of the coin. It may be as follows:

• Complexity of the model

• Risk of model error due to more complexity in the structure.

• Modelling daily temperature which is no less than a herculean task

Thus, in spite of the above mentioned flaws in the system, chances are high that weather derivatives shall help countries redeem themselves from the clutches of the mercurial rains and work towards strengthening of the economies, thereby, giving a fillip to droughts and floods.

Submitted By:

Ritika Yadav

In contrast to insurance, weather derivatives cover low risks and high probability events as per certain customised policies. Currently, energy companies and energy-related businesses use Weather Futures. However, there have been growing concerns and signs of potential growth in weather futures trading among agricultural firms and companies involved in tourism and travel as well. As such, India also has witnessed a welcome response to weather derivatives owing to the fluctuations in weather conditions. In India, Rainfall insurance has wide spread implications because despite the technological advancements, India has to depend on monsoon rains, with lack of irrigation. Still, it has been most often used in the U.S. and the U.K.

No doubt, this form of derivative trading is highly applicable in context with the present scenario but this carries along with it certain disadvantages as well for the daily models on the flip side of the coin. It may be as follows:

• Complexity of the model

• Risk of model error due to more complexity in the structure.

• Modelling daily temperature which is no less than a herculean task

Thus, in spite of the above mentioned flaws in the system, chances are high that weather derivatives shall help countries redeem themselves from the clutches of the mercurial rains and work towards strengthening of the economies, thereby, giving a fillip to droughts and floods.

Submitted By:

Ritika Yadav

Subsidies - The Double Edged Sword

Subsidies are a double-edged sword which every country professes to promote in the domestic economy but not without negative implications. Basically, subsidies are a form of financial assistance granted by the Government to a business or an economic sector (Source:Wikipedia). The most important effect of subsidies on the economy is the income redistributive effect. Subsidies are expected to provide some kind of monetary benefit to the underprivileged section of the society, thereby increasing their welfare. However, there could be other types of subsidies, which need not necessarily result in income redistribution: for example, export subsidies. These are typically given to encourage export oriented units, who would otherwise (i.e., without the benefit of subsidy) have to charge much higher prices because cost of production may be high due to smaller scale of production etc. If they charge higher prices, they will lose market and hence will die. So sometimes subsidies are provided to help some specific types of industries, because, they are supposed to lead to larger economic gains like increased foreign exchange earnings etc. Further, there could also be hidden subsidies like tax holidays for export oriented units or emerging sectors in the economy.

Notwithstanding whichever type of subsidy, they will all ultimately lead to resource redistribution in some or the other form. To illustrate it with an example, lets assume that an investor has 2 crore, which she intends to invest in some industry. Now, there are two options available to her : one, in an industry which doesnt receive any subsidy (eg: opening a motor car dealership) and two: an industry which involves some kind of subsidy ( eg. cold storage unit). It is most likely that the investor will choose to invest in the industry which enjoys a subsidy because her income will be more from the subsidized industry. Therefore, investments generally tend to flow to those areas, which have some kind of subsidy. But, considering the situation when the economy needs more motor car garages than cold storage, even though subsidies are available for cold storage, then investment is likely to flow to cold storage than motor car garages, though the other way would have been more desirable. So at times, the subsidies tend to alter the flow of resources to certain sectors from their competing sectors.

Usually, therefore, subsidies are given to those sectors, which the policymakers think need to have greater resource flow.

Since subsidies usually have income redistributing effects, they are widely favoured as a policy choice. If properly designed and implemented, subsidies can give a big boost to an industry or a sector (for instance, tax holiday to software exports led to the software boom in India).

However, subsidies are harmful, if they are poorly targeted or do not reach the intended beneficiaries. Two examples of this are the food subsidy and the fertilizer subsidy granted by the Government of India.

In case of food subsidy, the Government buys food grains at higher prices (called Minimum Support Prices). It enables the farmers to receive higher income, and then sell the same grains at lower prices (called Common Issue Prices) to poor people. Since it buys at higher price and sells at lower price, the difference will have to be borne by the Government as subsidy. This subsidy is called food subsidy. The annual food subsidy bill amounted to Rs 43627 crore in 2008-09 (Source:Public information bureau release). However, just 42% of the deserving people are benefited by it, according to a Planning Commission study released in 2008. A major portion of the allotted money is consumed in the system itself for example, the carrying costs of the Food Corporation of India.

Like-wise, in case of fertilizer subsidy also, it goes to support inefficient fertilizer companies (mostly public sector units). So, the two most important subsidies in India accounting for 4% and 3.5% of the GDP respectively are actually wastage of public money.

Moreover, if subsidies are financed by debt, the Government's debt liability increases. When the debt liability of the government increases, after a certain point, the Government's major part of revenues will go for interest payments, thereby leaving very little scope for developmental work. So subsidies have many drawbacks, if they are not implemented properly. This has led to lot of criticism against the subsidies in India and also across the world.

Submitted By:

Seeona Pani

Saturday, August 29, 2009

Sona he, Sada ke Liye!!

Gold investment worldwide has grown dramatically in the last five years, but compared with the total stock of financial assets, gold bullion investment is still just a tiny proportion.

Several factors are now stimulating gold investment by new pension fund money - as well as by private investors.

Several factors are now stimulating gold investment by new pension fund money - as well as by private investors.

Demand from New Gold Investment Markets

Sales of gold jewellery across Asia are surging as the local economies boom and private investment grows. China's gold investment demand grew by 20% in 2007, while Indian consumers bought a record 900 tonnes – well over one-fifth of the total world market.

Gold buyers in Asia tend to think of their jewellery as a form of gold investment. Prevented from owning gold bullion until very recently, they buy gold to protect their savings from inflation and currency shocks.

That's why the most popular form of gold jewellery in Asia – heavy chains and bracelets – is known as "investment jewellery" in the gold industry.

Gold Investment vs. the Falling Dollar

As the US Dollar has slumped gold investment has outstripped the gains in all major world currencies.

In the five years to 2008 buying Euros to defend against the Dollar's decline has returned 47%. Gold investment, on the other hand, has returned 131%.

British, Australian, South African and Indian citizens undertaking gold investments in 2007 all enjoyed the gold price reaching record new all-time highs.

When Inflation Looms, Gold Investment Shines

The surge in crude oil prices has closely matched the gains in gold prices since 2003, but many people now thinking about gold investment will also want to consider the surge in world food prices, the boom in base metals such as copper, and the current all-time highs in the cost of shipping.

Rising demand for better housing and durable goods from Asian consumers is certainly a factor. But many gold investment analysts also point to the huge growth in credit and debt in the West.

The money supply in the United States has doubled in the last seven years. In Europe, growth in the money supply hit a near-30 year record in late 2007, increasing the appeal of gold investment as the value of each Euro in circulation threatens to shrink under the weight of new notes and electronic account balances.

Gold Investment: The Antidote to Complex Debt Defaults

The global credit crunch first bit when the alphabet soup of MBS, CDOs, CDS and ABCP turned sour as the US mortgage market turned down.

These instruments thrive in the opaque, off-balance-sheet environment of modern financial engineering.

But transparency is important. The modern world has audited accounts, and open exchanges, and 'public' companies for a good reason: because previous generations understood that when investment stops being open and transparent, and reverts to cosy secret deals, complex contracts, and big executive bonuses, then it is general investors who get cheated. Transparency helps stop these problems developing.

In stark contrast to the burgeoning complexity of modern securities markets gold investment remains uniquely simple , and - dealt the right way - uniquely transparent.

A solid gold investment sets you free from the risk of credit default or banking failures.

Submitted by :

Bishakha Kumar

Green Shoots Vs Yellow Weeds

'Green shoots' has been a favorite phrase amongst economists in recent months, as the slowing momentum of global economic decline raises the hopes that recovery from the recession may be near . After the collapse of Lehman Brothers in September 2008, the global financial system nearly melted down and the world economy went into free fall. Infact, the rate of economic contraction in the fourth quarter of 2008 and the first quarter of 2009 reached near-depression levels.

Come mid-2009 many pundits are suggesting that the recent data from the manufacturing, housing market, labor markets suggest that the “green shoots” of an economic recovery are blossoming. These tentative green shoots that we hear so much about these days may well be overrun by yellow weeds even in the medium term, heralding a weak global recovery over the next two years. First, employment is still falling sharply in the US and other economies. Indeed, in advanced economies, the unemployment rate will be above 10% by 2010. This will be bad news for consumption and the size of bank losses.

Come mid-2009 many pundits are suggesting that the recent data from the manufacturing, housing market, labor markets suggest that the “green shoots” of an economic recovery are blossoming. These tentative green shoots that we hear so much about these days may well be overrun by yellow weeds even in the medium term, heralding a weak global recovery over the next two years. First, employment is still falling sharply in the US and other economies. Indeed, in advanced economies, the unemployment rate will be above 10% by 2010. This will be bad news for consumption and the size of bank losses.

Second, in countries running current-account deficits, consumers need to cut spending and save much more for many years. Shopped out, savings-less, and debt-burdened consumers have been hit by a wealth shock. Third, weak profitability, owing to high debts and low economic – and thus revenue – growth, and constant deflationary pressure on companies’ margins, will continue to constrain firms’ willingness to produce, hire workers, and invest. Fourth, rising government debt ratios will eventually lead to increases in real interest rates that may crowd out private spending.

Finally there is a risk that the increase in commodity prices might choke off a sustainable recovery if it weighs on industrial production and consumption. The recent increase in commodity prices, has contributed to an increase in the Baltic Dry shipping index. Moreover although trade finance is no longer quite as impaired as at the turn of the year, global trade continues to be quite weak as evidenced from recent data from China, the US and other countries.

In India’s case, benchmark equity index ,BSE sensex has soared 92 per cent from 2009 lows in early March, mainly driven by foreign fund inflows of almost $7 billion. India Inc has already raised Rs 5,000 crore from qualified institutional placements (QIPs) so far in 2009 and announced plans to raise another Rs 24,000 crore. The government today announced that industry output, as measured by the index of industrial production (IIP), grew 7 percent which may indicate that the decline in factory production has been arrested and adds to hopes of economic recovery.

Recently at the CEO round table organized by The Economic Times on the theme: Green Shoots or Yellow Weeds: Is the Recovery for Real? , Wipro chairman Azim Premji was heartened by the return of stability but warned that a runaway fiscal deficit could end up harming the economy. On the positive side , The panelists unanimously felt that India was on a strong wicket and that immense opportunities exist in the Indian market for companies to tap into.

To sum up, green shoots are more visible as of now but there are yellow weeds too. It is the duty of the governments and the central bankers to protect the green shoots and weed out bubbles. If they fail to do so, bubbles would impact the global economies badly.

Submitted by:

Sachin Matpal

Accelerating disinvestments of Public Sector Enterprises

When India launched measures to reform the economy in 1991, one of the items on its agenda was the restructuring of public sector enterprises. What this implied was that the ownership structure of PSEs had to change gradually from public ownership of equity shares to private holding. The process by which ownership change was to be brought about was through disinvestments.

If the public sector was perhaps necessary in the early stages of India’s economic development, disinvestment has become necessary and desirable – in the prevailing regime of liberalization. Firstly, because majority of the PSU firms are loss making which managed to survive only on the state financial support, thus, not only weakening the economy but were diverting badly need funds away from where they were badly needed. Secondly, it is desirable as resources released by disinvestment can make the State perform its basic functions efficiently, reduce the debt and interest burden. Therefore as recently seen the emphasis in the new economic policy changes is on the supply side, by deregulation and delicensing certain sectors,introducing tax reforms, and through disinvestments and privatization of PSEs.

If the public sector was perhaps necessary in the early stages of India’s economic development, disinvestment has become necessary and desirable – in the prevailing regime of liberalization. Firstly, because majority of the PSU firms are loss making which managed to survive only on the state financial support, thus, not only weakening the economy but were diverting badly need funds away from where they were badly needed. Secondly, it is desirable as resources released by disinvestment can make the State perform its basic functions efficiently, reduce the debt and interest burden. Therefore as recently seen the emphasis in the new economic policy changes is on the supply side, by deregulation and delicensing certain sectors,introducing tax reforms, and through disinvestments and privatization of PSEs.

Economic survey 2009 emphasized the unsustainability of fiscal deficit with borrowed funds. Such borrowed funds were being used for current revenue expenditure, and the casualty was infrastructure development.And it is supposed that if the momentum of disinvestments is maintained the government would be able to garner substantial amounts that should help reduce the whopping fiscal deficit which is 6.8 per cent of the GDP.

The recent issue of IPOs of NHPC and OIL alongwith the proposals for a host of companies waiting for the government nod for disinvestment include Bharat Sanchar Nigam Ltd (BSNL), railway consultancy firm RITES, National Aviation Company, and Ircon is all part of the government’s fund raising plans. However, one of the issues on which no clarity has emerged is the manner in which the unlisted PSUs will be allowed to tap the capital market with an initial public offer. One view is that allowing unlisted PSUs to tap the capital market would not necessarily result in any proceeds for the centre and not help meet the government’s fiscal deficit. Hence, such IPOs should be structured in a manner that will enable the government to also divest its stake and mobilise resources to reduce the fiscal deficit.

Another view is that PSU disinvestment should not be used as an instrument to meet the government fiscal deficit. Instead, it should be used to subject the PSUs to market discipline so that its management can measure its performance from its stock valuation in the open market. Such a view also supports more listed PSUs to float new stock to raise resources from a reviving stock market.

What will emerge out as an outcome of the current disinvestment procedure of the government is yet to be seen. But it is an irony indeed that the private companies in the rest of the nations are being rescued by the Government’s bailouts and in India the reverse is happening through disinvestment.

Jaya Roopwani

MBA(IB)2009-11

Monday, August 24, 2009

Cashonova Quiz- 9

Hi All,

Sorry for the delay in the Cashonova Quiz , but neways here goes.

Hope to have loads of replies:-

1.

Name the film, remember this is a finance quiz

2.

Connect the 3 visuals (you have to think a bit laterally for this)

3.

The above companies are 5th, 4th, 3rd and 2nd in a particular list. Who is 1st?

4.

What does the above graph represent?

5.

Name the character

6.

Logo of which organisation?

Sorry for the delay in the Cashonova Quiz , but neways here goes.

Hope to have loads of replies:-

1.

Name the film, remember this is a finance quiz

2.

Connect the 3 visuals (you have to think a bit laterally for this)

3.

The above companies are 5th, 4th, 3rd and 2nd in a particular list. Who is 1st?

4.

What does the above graph represent?

5.

Name the character

6.

Logo of which organisation?

7. This is a term coined during the financial crisis to describe a situation where the unemployment rate among men is far greater than that amongst women. What is this term called?

8.

----- Traders is a slang term to describe investors who look to trade in high - risk investments. ------ Traders prefer to invest in riskier endeavours and seek higher risk premium as they go on.Fill in the blanksFriday, August 21, 2009

Drought- A Painful State

India’s vast farming economy is on the verge of crisis because of the drought that has hit the entire country this year. Out of the 604 districts 161 has been declared drought prone and the sowing of crops nationally has reduced by 20%. This fear of drought has pulled down the sensex by 626 points. Many economists have predicted that this drought will have a downward revision on the India’s growth rate of GDP.

Agriculture and allied activities accounts for a significant share in India’s GDP (17%), with over 60% population earning their livelihood via these activities. Drought has a direct impact on the production and the price of agri goods. Over 50% of the population that depends on agriculture and allied activities are marginal farmers or producers. Its expected that production of rice will fall by 10 million tons this year. This loss in production will lead to higher price, and marginal farmers or producers will end up buying goods at higher price to meet their basic amenities.

Agricultural Labourers are feeling the pain too. Due to low production, employment will also be severely affected. It has also been said that share of agriculture in rural income is down to about 40%. This will affect a large section of the population in India.

Its also feared that the season may turn out to be as bad as 2004 when the GDP fell by 1% from 8.5% to 7.5% due to similar causes. But this prediction of downward revision is likely to be proved wrong. It is predicted that India’s GDP will still grow at the rate close to 7% this year as predicted earlier.

Forecasting the impact that drought can have on our economy, government is taking drought relief measures that will protect the rural income and in turn help in lowering the impact of drought on growth rate.

Though economists are divided whether the drought will have much impact on the GDP or not, any impact on the production and price due to drought will have a direct impact on the employment and demand which in turn negatively affect GDP. Surely, drought is a serious issue that the government is facing. Relying on the old buffer stock for consumption problem may be a short term solution to the problem of drought, but it’s time for the government officials to put on their thinking caps on and take some substantial steps to cure this problem.

Submitted By:

Neha Daga

Chetan Raghav

It's All Less Taxing Now

{kind=link}

Our finance minister, Mr. Pranab Mukherjee released the draft of the long awaited Direct tax code to be implemented from year 2011 on Wednesday,12th August,2009 . The new tax code represent a radical review of the Income-Tax Act, 1961 which is in operation right now. It marks a paradigm shift in the Tax structure of our country.

Taxes serve the main objective of financing government expenditure. There used to be a time when there were 11 different tax-rates depending on the income of an individual. The rates used to be as high as 97.75% of the total income of an individual. Naturally, most of the people tried to evade taxes. Even now, when the tax structure has been eased a lot, people try to evade taxes. Now consider the situation, after this tax code will be implemented-The tax rate for people having income from 1.6 lakh-10 lakh is only 10% which means that majority of Indians will be paying only 1/10th of their earnings. So the basic motive behind changing the existing tax structure is to simplify the tax procedures by introducing moderate level of taxation and expanding the tax base.

The tax rate slabs have been expanded with an assumption that more people will be encouraged to pay taxes now. Prima facie, tax structure looks to be quite impressive-The slabs for individuals have been drastically changed. It proposes to tax incomes up to Rs 10 lakh at 10%, that between Rs 10 lakh and Rs 25 lakh at 20% and sum in excess of that at 30% which is in sharp contrast to complicated tax structure applicable now-a-days. For someone earning say, Rs 14.5 lakh per year, the new numbers could look something like this: Rs 1.6 lakh (basic exemption) Rs 3 lakh (saving) Rs 9.90 lakh taxable income, tax rate for Rs 10 lakh = 10 per cent Tax liability = Rs 99,000. Looks brilliant, but the tricky part lies in the fact that all the perks that an employee used to enjoy in his salary will now be brought under the tax net. This means the taxable income will now be higher. But on the whole, new tax structure stands to benefit middle-class.

One good news for students pursuing higher education through loans is that the term ‘higher education’ has been enlarged to include full-time studies in graduate or postgraduate course for the purpose of deductions under savings. Also, there will be no more any confusion between AY(Assessment Year) and PY(Previous Year), now only FY, i.e financial year will be used. The tax draft has also tried to make the corporate sector happy. The tax rate on profits of the company has also been decreased from 30% to 25%.

The new tax structure basically aims at encouraging the idea of savings among people and at the same time leaving more disposable income in hands of people for the purpose of increasing consumption in the times of recession. Apart from this, the new tax code also tries to reduce the incidence of tax avoidance. It has incorporated a whole chapter on provisions to prevent tax-evasions. Taking into account all these, the new tax code looks to be a well-structured, comprehensive and better tax structure that was much needed in India’s quest to be a developed nation. The only thing to be seen now is how successfully will this new tax structure be implemented and adopted by government and people of our country.

Contributed By:

Arun Singhal

Opportunities In Distress!

Recession is possibly the best time to launch a new business, expand an existing one or get ahead in career if you understand the importance of creating and delivering genuine value during the time when people need it the most!!

It’s true that during a recession, the media turns a little bit of negativity into a mountain of pessimism. This makes a lot of people financially paranoid. People become socially conditioned to expect the worst. If you buy into this social hysteria, you become a victim too. But if you tune out such panic and maintain a grip on rational thought, you’ll see some amazing opportunities popping up everywhere you look.

During such times people get scared and start cutting back on expenses. They stop buying stuff they don’t need, or ostensibly as they are made to think so! This causes some companies to do poorly, especially companies that don’t provide the value that we really need. We can put off non-essentials and live without new credit cards and fuel-guzzling SUVs for a while.

We become more sensitive to receiving genuine value. When we spend money, we want to make sure that we are getting a fair deal. Consequently, businesses that provide genuine value can actually do better during a recession. More and more people will flock to those businesses in tough times, while the fluff companies will only be on a downward spiral.

Companies trying to extract money without providing fair value in exchange find it tough to survive a recession. Many of the dead or dying financial companies are like that. Recession helps to weed out the companies that are not creating and delivering value. Many of those companies were doing a good job at one time, but they failed to keep pace. Companies that cannot adapt to changing values deserve to die off, and are replaced by new companies that have a better sense of people’s current needs and desires.

The need of the hour is to create and deliver genuine value, because that is what is going to help a company rise above recession and sustain its growth over the years. And History testifies that, the ones which could weather, could last!

Submitted By:

Mehak Gandhi

Saturday, August 15, 2009

Cashonova Quiz 8 with Answers

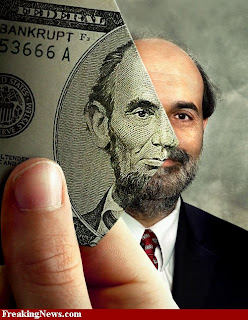

1) Whose face is hidden behind the note?

Ans)Ben Bernanke

2) Connect

Connect

Ans)All have currencies named after them. Simon Bolivar (Bolivia and Venezuela) , Hernandez Balboa (Colombia) and Quetzel (Guatemala)

3) What currency is this?

Ans) Pound

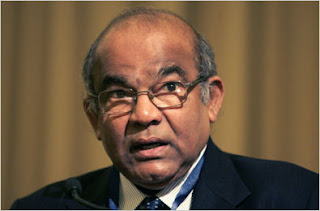

4) Identify the 2 gentlemen and tell me who comes next in the list?

Ans)D Subbarao, these 2 are Bimal Jalan and YV Reddy

5)

The lady above is a parody of a financial institution. Name the financial institution.

Ans)Bank of England

6) What was Five Hundred Thousand called in the old Persian number system?

Ans)Crore

7)

This is a film poster, of a film named after an institution which is of high significance particularly in the history of insurance. Name the institution.

Ans)Lloyds of London

8)"His income and PAN card would help. Even if you have below taxable income,then also you can get a PAN card. So, one should apply for a card, aswithout it one cannot get return of income," said Agarwal. This is a statement made by the father, of a young boy in Orissa who was signed up by a voluntary organization as a model. Who is this boy, and what is his significance in the history of finance?

Ans)Ayush Ranjan Rout, youngest PAN card holder

Ans)Ben Bernanke

2)

Connect

Connect

Ans)All have currencies named after them. Simon Bolivar (Bolivia and Venezuela) , Hernandez Balboa (Colombia) and Quetzel (Guatemala)

3) What currency is this?

Ans) Pound

4) Identify the 2 gentlemen and tell me who comes next in the list?

Ans)D Subbarao, these 2 are Bimal Jalan and YV Reddy

5)

The lady above is a parody of a financial institution. Name the financial institution.

Ans)Bank of England

6) What was Five Hundred Thousand called in the old Persian number system?

Ans)Crore

7)

This is a film poster, of a film named after an institution which is of high significance particularly in the history of insurance. Name the institution.

Ans)Lloyds of London

8)"His income and PAN card would help. Even if you have below taxable income,then also you can get a PAN card. So, one should apply for a card, aswithout it one cannot get return of income," said Agarwal. This is a statement made by the father, of a young boy in Orissa who was signed up by a voluntary organization as a model. Who is this boy, and what is his significance in the history of finance?

Ans)Ayush Ranjan Rout, youngest PAN card holder

Tuesday, July 28, 2009

Panel Discussion on Union Budget 2009

The Finance Club organized the panel discussion on Union Budget 2009, on July 8th 2009.

The eminent panelist and enthusiastic interaction by the audience made the event a great success!!!

The details of the event are as undersaid.

A Budget of Intent not Content

The Union Budget of 2009-10 has been met with mixed responses from industry, stock market, academia and the common man. The stock market has plummeted down at an alarming rate since the Budget announcement, fuelled by a large gap between the expectations of corporate India and actual measures taken in the Budget. The Budget has been perceived as one targeted majorly at the common man, and it has evoked a skeptical reaction in the main, from India Inc. It is seen as one aimed at the long term, rather than on immediate reforms. Th ese sentiments were echoed in a thought provoking and enlightening panel discussion on the Budget at Indian Institute of Foreign Trade, Kolkata on 8th July , where the general consensus was that it was a ‘A Budget of Intent rather than Content’.

ese sentiments were echoed in a thought provoking and enlightening panel discussion on the Budget at Indian Institute of Foreign Trade, Kolkata on 8th July , where the general consensus was that it was a ‘A Budget of Intent rather than Content’.

The discussion was moderated by Professor Ranajoy Bhattacharya from IIFT, a Fullbright scholar and a prominent name in the economics field. The distinguished panel included Mr. Basant Maheshwari, a full-time investor and stock market expert for EquityDesk.com, Mr. Anirban Ganguly, Sr. Manager of Taxation at KPMG , Dr. Dipankar Das Gupta, renowned economist and former head of the Indian Statistical Institute & Mr. Asrujit Mandal from KPMG, a Tax and Regulatory matter expert.

Mr Maheshwari, underplayed the impact of the Budget on the stock market, calling it ‘a catalyst for the market to act as it wants to do’. He agreed that the effect was more short term, as within two weeks the stock market would be back looking at the Dow Jones and individual company results. He appreciated the fact that the changes that the government was trying to implement were good from the long term perspective, and this budget promised dramatic changes in the subsidy structure. However he did voice concerns about the large fiscal deficit as well as the insignificant disinvestment measures taken by the government. He summed up the budget as one which showed the Finance Minister as an ‘accountant rather than a visionary’.

Mr Mandal and Mr Ganguly gave an eye opening analysis of the budget from the taxation perspective. While Mr Mandal dissected the budget from the point of view of direct tax, Mr Ganguly gave an indirect tax perspective on the budget. Mr Mandal expressed confidence about the resilient nature of the Indian economy. However he did express the view that with no changes in corporate surcharge and increase in MAT, the industry had little to cheer. He felt that the priorities enumerated in the Economic Survey should be implemented, specifically the return to fiscal prudence and the revitalization of divestment programs. Mr Ganguly felt that it was imperative that India has a smooth transition to the GST(Goods & Services Tax) era. He expressed his concern on the lack of a proper timeline or framework for various phases of GST implementation. However, he did sound positive about the simplification of refund schemes for export services and the enhanced coverage of taxes.

The final speaker of the session was Mr Dipankar Dasgupta who gave an insight into the budget from an economist’s perspective. He pointed out a major anomaly in the finance minister’s statement during the budget session where the finance minister had quoted that the principal growth driver during the previous UPA government’s reign was private investment, where as in reality private sector growth has been on a downturn since the UPA came into power in 2004.

He lauded few of the measures undertaken by the government especially the Rajiv Gandhi Rural Electrification Scheme and the NREGA. However, the achievement of the objectives of these schemes remained in doubt due to the large fiscal deficit. Professor Dasgupta shed light on some alarming trends in the government’s planned and nonplanned expenditure, especially in the education, health and defence sectors. His discussion revealed the fact that perhaps the government’s expenditure was not targeted in the right direction. Maintainence of schools, hospitals in villages remains neglected while there is huge expenditure on purchase of weaponry every year. In his opinion the budget was more a political document than one which promised growth of the economy.

In the interactive session which followed, the panelists discussed a variety of issues from fiscal deficit to comparisons between India’s and China’s economy. One significant point made by Mr Maheshwari was that the emphasis on development at the Bottom of the Pyramid, which has been frowned upon by many in India Inc, is actually great news for the consumer sector,. Schemes such as NREGA would increase the consumption power of the poorest of the poor, and hence lead to higher sales for the companies. Another thought expressed worth pondering upon was the view that perhaps India is moving towards the China Model of growth , wherein you build infrastructure first and then invite investment.

In all, the panel came to a consensus that the Budget should be looked as one with honorable intentions for India’s development, rather than one which promised immediate results.

The Union Budget of 2009-10 has been met with mixed responses from industry, stock market, academia and the common man. The stock market has plummeted down at an alarming rate since the Budget announcement, fuelled by a large gap between the expectations of corporate India and actual measures taken in the Budget. The Budget has been perceived as one targeted majorly at the common man, and it has evoked a skeptical reaction in the main, from India Inc. It is seen as one aimed at the long term, rather than on immediate reforms. Th

ese sentiments were echoed in a thought provoking and enlightening panel discussion on the Budget at Indian Institute of Foreign Trade, Kolkata on 8th July , where the general consensus was that it was a ‘A Budget of Intent rather than Content’.

ese sentiments were echoed in a thought provoking and enlightening panel discussion on the Budget at Indian Institute of Foreign Trade, Kolkata on 8th July , where the general consensus was that it was a ‘A Budget of Intent rather than Content’.The discussion was moderated by Professor Ranajoy Bhattacharya from IIFT, a Fullbright scholar and a prominent name in the economics field. The distinguished panel included Mr. Basant Maheshwari, a full-time investor and stock market expert for EquityDesk.com, Mr. Anirban Ganguly, Sr. Manager of Taxation at KPMG , Dr. Dipankar Das Gupta, renowned economist and former head of the Indian Statistical Institute & Mr. Asrujit Mandal from KPMG, a Tax and Regulatory matter expert.

Mr Maheshwari, underplayed the impact of the Budget on the stock market, calling it ‘a catalyst for the market to act as it wants to do’. He agreed that the effect was more short term, as within two weeks the stock market would be back looking at the Dow Jones and individual company results. He appreciated the fact that the changes that the government was trying to implement were good from the long term perspective, and this budget promised dramatic changes in the subsidy structure. However he did voice concerns about the large fiscal deficit as well as the insignificant disinvestment measures taken by the government. He summed up the budget as one which showed the Finance Minister as an ‘accountant rather than a visionary’.

Mr Mandal and Mr Ganguly gave an eye opening analysis of the budget from the taxation perspective. While Mr Mandal dissected the budget from the point of view of direct tax, Mr Ganguly gave an indirect tax perspective on the budget. Mr Mandal expressed confidence about the resilient nature of the Indian economy. However he did express the view that with no changes in corporate surcharge and increase in MAT, the industry had little to cheer. He felt that the priorities enumerated in the Economic Survey should be implemented, specifically the return to fiscal prudence and the revitalization of divestment programs. Mr Ganguly felt that it was imperative that India has a smooth transition to the GST(Goods & Services Tax) era. He expressed his concern on the lack of a proper timeline or framework for various phases of GST implementation. However, he did sound positive about the simplification of refund schemes for export services and the enhanced coverage of taxes.

The final speaker of the session was Mr Dipankar Dasgupta who gave an insight into the budget from an economist’s perspective. He pointed out a major anomaly in the finance minister’s statement during the budget session where the finance minister had quoted that the principal growth driver during the previous UPA government’s reign was private investment, where as in reality private sector growth has been on a downturn since the UPA came into power in 2004.

He lauded few of the measures undertaken by the government especially the Rajiv Gandhi Rural Electrification Scheme and the NREGA. However, the achievement of the objectives of these schemes remained in doubt due to the large fiscal deficit. Professor Dasgupta shed light on some alarming trends in the government’s planned and nonplanned expenditure, especially in the education, health and defence sectors. His discussion revealed the fact that perhaps the government’s expenditure was not targeted in the right direction. Maintainence of schools, hospitals in villages remains neglected while there is huge expenditure on purchase of weaponry every year. In his opinion the budget was more a political document than one which promised growth of the economy.

In the interactive session which followed, the panelists discussed a variety of issues from fiscal deficit to comparisons between India’s and China’s economy. One significant point made by Mr Maheshwari was that the emphasis on development at the Bottom of the Pyramid, which has been frowned upon by many in India Inc, is actually great news for the consumer sector,. Schemes such as NREGA would increase the consumption power of the poorest of the poor, and hence lead to higher sales for the companies. Another thought expressed worth pondering upon was the view that perhaps India is moving towards the China Model of growth , wherein you build infrastructure first and then invite investment.

In all, the panel came to a consensus that the Budget should be looked as one with honorable intentions for India’s development, rather than one which promised immediate results.

Thursday, July 9, 2009

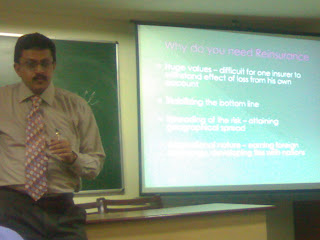

Guest Lecture- Rediscovering Insurance in the Lost Continent

The Finance club at IIFT Kolkata, organized the guest lecture on Reinsurance, on July 4, 2009. Here is the brief on the event.

Viewers can post their comments in the comment section!

In an era where insurance claims have reached astronomical proportions , Reinsurance has emerged as an integral part of the entire insurance framework. It is almost impossible for a single insurer to withstand all the claims from his own account. Reinsurance or the insurance of insurance helps insurance companies to spread their risk & stabilize their bottom line. With its rising importance in the financial sector, reinsurance has also emerged as an exciting career option.

In an era where insurance claims have reached astronomical proportions , Reinsurance has emerged as an integral part of the entire insurance framework. It is almost impossible for a single insurer to withstand all the claims from his own account. Reinsurance or the insurance of insurance helps insurance companies to spread their risk & stabilize their bottom line. With its rising importance in the financial sector, reinsurance has also emerged as an exciting career option.

The Lost Continent, Africa has not been left untouched by the phenomenon of reinsurance and the company spearheading Africa’s growth in this arena is African Reinsurance Corporation, the largest reinsurer in the continent. Mr Souvik Banerjea, a senior underwriter from the African Reinsurance Corporation shed light on various aspects of this growing field and the world of insurance in general, in an invigorating guest lecture at Indian Institute of Foreign Trade, Kolkata.

Mr Banerjea has a wealth of experience in this area, both in India and abroad, having previously worked for over 20 years in New India Assurance, with a 4 year stint in Japan, before moving on to Nairobi to work for the African Reinsurance Corporation. He shared his vast experience with the students of IIFT, who were introduced to a hitherto lesser known but emerging area in the gamut of finance. The session covered various aspects of insurance, from its genesis in the days of yore with bottomry bonds to new age concepts like alternative risk transfer. Financial instruments like Multi Line Products, Multi Trigger Products and Insurance Derivatives which have gained importance in the recent past were discussed. Of course the focus of the session was Reinsurance, whereby an insurance company transfers its risk to a reinsurer. This obviously reduces the risk undertaken by the insurer. Reinsurance being a primarily international phenomenon, not having caught on adequately in India helps insurance companies to diversify their risk geographically. Reinsurance also empowers insurance companies to take on larger risks and develops relations between insurers. Reinsurance can be done either through treaties entered into at the beginning of a period whereby the reinsurer examines the portfolio & future potential of the insurance company and sets a price , or on a facultative or case by case basis, wherein performance of the individual risk is considered along with safety measures and management of risk, before setting a price, this is especially done in the case of large risks.

Apart from enlightening the students on insurance and reinsurance , in particular Mr Banerjea also awakened students to career prospects in Africa. People generally carry a very negative impression about working in Africa, but Mr Banerjea did a great deal to dispel any inhibitions that students had in this regard. Rather, Africa is a place where there is great potential for growth and the very fact that it has not been explored to a great extent , makes it an exciting career destination.

The session aptly demonstrated the importance of and the high growth prospects in the field of Reinsurance , and also awakened students to the fact that Africa may well be the next frontier, as far as carving out a great career is concerned.

Viewers can post their comments in the comment section!

In an era where insurance claims have reached astronomical proportions , Reinsurance has emerged as an integral part of the entire insurance framework. It is almost impossible for a single insurer to withstand all the claims from his own account. Reinsurance or the insurance of insurance helps insurance companies to spread their risk & stabilize their bottom line. With its rising importance in the financial sector, reinsurance has also emerged as an exciting career option.

In an era where insurance claims have reached astronomical proportions , Reinsurance has emerged as an integral part of the entire insurance framework. It is almost impossible for a single insurer to withstand all the claims from his own account. Reinsurance or the insurance of insurance helps insurance companies to spread their risk & stabilize their bottom line. With its rising importance in the financial sector, reinsurance has also emerged as an exciting career option.The Lost Continent, Africa has not been left untouched by the phenomenon of reinsurance and the company spearheading Africa’s growth in this arena is African Reinsurance Corporation, the largest reinsurer in the continent. Mr Souvik Banerjea, a senior underwriter from the African Reinsurance Corporation shed light on various aspects of this growing field and the world of insurance in general, in an invigorating guest lecture at Indian Institute of Foreign Trade, Kolkata.

Mr Banerjea has a wealth of experience in this area, both in India and abroad, having previously worked for over 20 years in New India Assurance, with a 4 year stint in Japan, before moving on to Nairobi to work for the African Reinsurance Corporation. He shared his vast experience with the students of IIFT, who were introduced to a hitherto lesser known but emerging area in the gamut of finance. The session covered various aspects of insurance, from its genesis in the days of yore with bottomry bonds to new age concepts like alternative risk transfer. Financial instruments like Multi Line Products, Multi Trigger Products and Insurance Derivatives which have gained importance in the recent past were discussed. Of course the focus of the session was Reinsurance, whereby an insurance company transfers its risk to a reinsurer. This obviously reduces the risk undertaken by the insurer. Reinsurance being a primarily international phenomenon, not having caught on adequately in India helps insurance companies to diversify their risk geographically. Reinsurance also empowers insurance companies to take on larger risks and develops relations between insurers. Reinsurance can be done either through treaties entered into at the beginning of a period whereby the reinsurer examines the portfolio & future potential of the insurance company and sets a price , or on a facultative or case by case basis, wherein performance of the individual risk is considered along with safety measures and management of risk, before setting a price, this is especially done in the case of large risks.

Apart from enlightening the students on insurance and reinsurance , in particular Mr Banerjea also awakened students to career prospects in Africa. People generally carry a very negative impression about working in Africa, but Mr Banerjea did a great deal to dispel any inhibitions that students had in this regard. Rather, Africa is a place where there is great potential for growth and the very fact that it has not been explored to a great extent , makes it an exciting career destination.

The session aptly demonstrated the importance of and the high growth prospects in the field of Reinsurance , and also awakened students to the fact that Africa may well be the next frontier, as far as carving out a great career is concerned.

Contributed by Titash

Tuesday, July 7, 2009

Fact

Total expenditure in the first budget of independent India was 193 crore Rs. which has skyrocketed to 10 lac crore Rs in the latest budget ...... Its the first time 10 lac water mark has been breached ..

:) ravi

:) ravi

Monday, July 6, 2009

Welcome 2009-11

Hi,

I take this opportunity to welcome all the students of the batch 2009-11, on the behalf of the finance club of IIFT Kolkata.

We look forward for a great participation and see club as a useful forum for enriching our knowledge.

Bablish Joshi.

Club Coordinator,

Cashonova,

I take this opportunity to welcome all the students of the batch 2009-11, on the behalf of the finance club of IIFT Kolkata.

We look forward for a great participation and see club as a useful forum for enriching our knowledge.

Bablish Joshi.

Club Coordinator,

Cashonova,

Links on Budget

http://www.bloomberg.com/apps/news?pid=20601091&sid=a9aeWosOf7lU

http://www.premiuminvestments.in/cover-feature-33310/106/Lack-of-policy-announcement-disappoints-market.html

http://www.bloomberg.com/apps/news?pid=20601091&sid=ao45ObpLTXF4

http://in.reuters.com/article/businessNews/idINIndia-40829720090706?sp=true

http://online.wsj.com/article/SB124686565473099541.html

http://www.premiuminvestments.in/cover-feature-33310/106/Lack-of-policy-announcement-disappoints-market.html

http://www.bloomberg.com/apps/news?pid=20601091&sid=ao45ObpLTXF4

http://in.reuters.com/article/businessNews/idINIndia-40829720090706?sp=true

http://online.wsj.com/article/SB124686565473099541.html

Sunday, March 1, 2009

Picture Quiz

Hello Friends. I am back again with my picture quiz. Not much chance of googling though can be easily worked out. There are eight questions in all and I am sure the winner will surely get 'em all. Mail your answers to cashonovaclub@iift.ac.in by Tuesday midnight. Happy Quizzing!!!

1.) Identify the missing link (good one)

???? ????

???? ????

Agilent Technologies(A), Bombardier Inc(B), Citigroup(C), Dominion Resources(D), Eni SpA(E), Ford Motors(F), Genpact(G). NYSE Tickers. Ford Motor Corp is the answer.

2.) Identify this very famous man (sitter)

Mohammad Yunus

3.) Identify the logo (its on the tip of your tongue)

Commonwealth Bank

4.) Identify the company for which this ad was published

(Mind you this is not entirely finance)

Maytas Hill County. Maytas would have done.

5.) Connect them (hmmm...no hints. workable)

Dabhol, Arthur Andersen and Enron(Jeffrey Skilling and Kenneth Lay) - Rest connect yourself

6.) Identify the book and the author (should be easy)

Hot, Flat and Crowded

7.) Identify the logo (think without googling)

Allianz - The Insurance Group

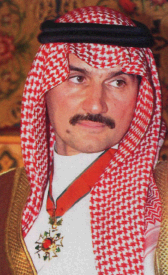

8.) Identify this very famous man (though not without controversies)

Prince Al-Waleed. The Warren Buffet of Saudi Arabia.

1.) Identify the missing link (good one)

???? ????

???? ????

Agilent Technologies(A), Bombardier Inc(B), Citigroup(C), Dominion Resources(D), Eni SpA(E), Ford Motors(F), Genpact(G). NYSE Tickers. Ford Motor Corp is the answer.

2.) Identify this very famous man (sitter)

Mohammad Yunus

3.) Identify the logo (its on the tip of your tongue)

Commonwealth Bank

4.) Identify the company for which this ad was published

(Mind you this is not entirely finance)

Maytas Hill County. Maytas would have done.

5.) Connect them (hmmm...no hints. workable)

Dabhol, Arthur Andersen and Enron(Jeffrey Skilling and Kenneth Lay) - Rest connect yourself

6.) Identify the book and the author (should be easy)

Hot, Flat and Crowded

7.) Identify the logo (think without googling)

Allianz - The Insurance Group

8.) Identify this very famous man (though not without controversies)

Prince Al-Waleed. The Warren Buffet of Saudi Arabia.

Wednesday, February 25, 2009

List of Tentative Electives for Finance Major

- Project Appraisal & Finance

- Security Analysis & Portfolio Management

- Management of Financial Services

- Retail Banking

- Fixed Income Security / Analytics

- Derivatives & Risk Management

- Financial Market & Instruments

- Equity Research & Analysis

- Corporate Restructuring

- Infra Structure Financing

- Insurance

- Strategic Financial Management

- Business Analysis And Valuation

- Management of Financial Institutions

- Tax Planning

- Stochastic Calculus in finance

- International Financial markets

- Asset Securitization

- Market Microstructure

- Behavioural Finance

Please post your comments for the electives , as a trail, under the Post.

Saturday, February 21, 2009

Cashonova Quiz 6

Hi Guys, I am back with the 6th edition of the Cashonova quiz series

Hope to have an enthusiastic response once again.

1.

2.

Connect the two images below

3.

This man, from the world of business & technology had a special affinity for a particular letter.

Identify him( Clue :- Oscars)

4.

A very famous company is named after this Greek Goddess. Identify her

5.

Hope to have an enthusiastic response once again.

Your QuizMaster-- Titash

Please send in your answers by 22 Feb 2009, 11:59:59

@ cashonovaclub@iift.ac.in

1.

This is the logo for a product which has emerged as a major rival to one of the most popular products of the 21st century. What?

2.

Connect the two images below

3.

This man, from the world of business & technology had a special affinity for a particular letter.

Identify him( Clue :- Oscars)

4.

A very famous company is named after this Greek Goddess. Identify her

5.

On June 23, 2006, it received from the U.S. Food & Drug Administration a 180-day exclusivity period to sell simvastatin in the U.S. as a generic drug at 80 mg strength. It presently competes with the maker of brand-name Zocor, Merck & Co.; Teva Pharmaceutical Industries, which has 180-day exclusivity at strengths other than 80 mg.Which company am I talking about?

6.

The term and service was introduced by a Bengali entrepreneur Sake Dean Mahomed, who opened a bath known as 'Mahomed's Indian Vapour Baths' in Brighton, England in 1759. His baths were like Turkish baths where clients received an Indian treatment of therapeutic massage.What is this term?

7.

It is the largest Russian company . After acquisition of the oil company Sibneft.With 119 billion barrels of reserves, ranks behind only Saudi Arabia, with 263 billion barrels, and Iran, with 133 billion barrels, as the world's biggest owner of oil and oil equivalent in natural gas

8.

Connect

Subscribe to:

Posts (Atom)