Harsimran Singh Sahni

Indian Institute of Foreign Trade

Kolkata Campus

Email-

harsimransahni@gmail.com

The Collapse of Lehman Brothers

This was an economic 9/11!!

On September 15, 2008, Lehman Brothers filed for bankruptcy with $639 billion in assets and $619 billion in debt, Lehman's bankruptcy filing was the largest in history, surpassed Enron and WorldCom, which induced the financial crisis that swept through global financial markets in 2008.

The History of Lehman Brothers

Lehman Brothers, the largest investment bank, roots are traced back to a small general store founded by German immigrant Henry Lehman in Montgomery, Alabama, in 1844. In 1850, Henry Lehman and his brothers, Emanuel and Mayer, founded Lehman Brothers which was primarily involved in Investment Banking, equity and fixed income sales, research and trading. It was primary dealer in US Treasury securities market.

It has emerged stronger as it faced the plenty of challenges but it survived all- the railroad bankruptcies of 1800, the Great Depression of 1930s, Two World Wars. Despite its ability to survive the major challenges, it filed for the largest bankruptcy in US history on 15 September 2008.

Build-up to the Collapse

Mathematical Model for Money Making

From about 2001 and onwards, a credit bubble started to appear in the United States. Huge amount of capital moved into the country, in search of profit higher than the low rate of interest that existed at the time and at the same time, housing bubble was also in the making; and through the process of securitization the housing market was closely linked to the credit bubble in the U.S. financial system. The team of maths and physics PhDs showed, then CEO Dick Fuld, the calculations that how the bank will end up in profits if they invest in real markets and the next five years saw the bank borrowing billions of dollars to invest in housing market.

Lehman Brothers started giving insurance to the banks that have offered loans to customers and accepted that the chance of default on loans would be 5%. If 100 customers borrowing $1million have 5% assumed chance of default, given the interest rate @5%, the next year's $5 million would be worth 5/(5/100+1)=5/1.05=4.76 million now. So banks would have to pay minimum $4.76 million for insurance and to make money, Lehman Brothers would double the price to $9.5 million and expect to make $4.76 million out of each of these deals. And if more than ten of them default, the banks had to pay premium only for ten customers and the rest will be bear by Lehman Brothers. This type of deal is called Collateralised debt obligation contract in which the Lehman Brothers’ offering is senior tranche of CDO and one you are getting is junior tranche of CDO.

As it was unlikely to have more than ten borrowers defaulting, Lehman don’t have to pay anything and just pocketing the premium and it was considered as the safe investment as government deposits.

Pitfalls in Model

CDO is lot more risky than bank deposits, but Lehman Brothers didn’t realized them. The first source of error was that that they have assumed that each investor has 5% chance of default from historical data. There hasn't been a national drop of housing price since the great depression in the 1920s, so the chance that a borrower defaults was calculated on the basis of a good period when the housing prices surged. However, the housing market crashed in 2007 and to worsen this, 22% of these borrowers are sub-prime borrowers, those who had little income and had little hope of returning money which made lending quite risky.

The second source of error is that whether you make money from selling the CDO insurance for the bank depends on whether the borrowers return the money, which in turns depends on the economy. So if the economy goes down, you are a lot more likely to lose money. These two errors were sufficient to mask the risk in CDO.

Major cause of the Collapse- Subprime mortgage crisis

One novelty about housing bubble was that it involved the new group of economic actors: people who for the first time were able to buy house-subprime borrowers. In 2005 and 2006 Lehman was the largest producer of securities based on subprime mortgages.

The moment the market turned down, however, they would have to foreclose and securities based on this type of mortgage would register a loss. This is exactly what happened in August 2007 when the decline of US housing market started to register in major way in financial systems and major mortgage outfit went under and the amount of subprime mortgages was estimated at $2 trillion.

The indices came to play a crucial role in transforming a situation of economic loss in the housing market into a low level panic in the parts of financial system along with a lack of information about the location of the risks. However, it allowed investors to realize that the market was now lowering the price on securities based on subprime mortgages, they didn’t allowed the investors to figure out which securities were of low quality and which were not. The result was the fear about the hidden losses spread to all subprime mortgage-related bonds and CDO as well as to the institutions.

In 2007, due to the poor market conditions in mortgage space necessitated the substantial reduction in its resource and capacity and the firm closed its subprime lender, BNC Mortgage. As 2007 became 2008, during the months after the fall of Bear Stearns the general economic situation continued to worsen and value of many assets had fallen dramatically and the pressure shifted to another investment banks especially to Lehman. In 2nd fiscal quarter, Lehman reported losses of $2.8 billion and forced to sell $6 billion assets which further panic the investors, who feared that Lehman had quite a bit more of hidden losses.

Financial Market Fallout

The Lehman bankruptcy act as kind of detonator and set off the panic which ended up threatening not only US Financial system but also global financial system. Some of the institution owned Lehman bonds and were engaged in credit default swaps with Lehman which had direct effect of Lehman bankruptcy. But the indirect effects of Lehman bankruptcy were caused by the fear and rumours that now begin to circulate and were more dangerous than direct effects. This was the $613 billion bankruptcy, largest ever in US history. There were nearly eighty Lehman subsidiaries around the world that had close ties with US parent company which ensured that fallout of Lehman will immediately spread all over world.

Fig-1. Short Term and Long Term Trends of Global Economy

In Japan, the banks and insurance companies announced the losses $2.4 billion because of ties with Lehman. Similarly, Iceland’s financial institutions were very much hurt by spike in CDSs that followed Lehman’s fall. Fed and Treasury failed to realize that major actor Primary Fund, which held $785 million in Lehman bonds became worthless overnight which set off a run on money market. The existence of investments in Lehman bonds in one market firm made investors think that other money market firms might have Lehman bonds or hidden losses. The direct link to one actor, led to belief that all the actors in the market might have similar holdings having indirect effect. UBS AG suddenly lost $4 billion due to rumours whereas actual figure stood $300 million. (Fig-1)

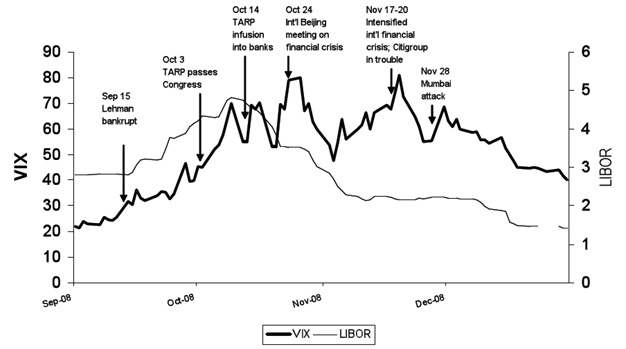

The process of financial disintegration that was set off by Lehman accelerated during the fall of 2008. The LIBOR-OIS spread peaked in mid October until decision was announced to invest TARP money directly into US banks and the fear Index shot up as well. (Fig-2)

Fig-2. Fear Index (VIX) and LIBOR during the Financial Crisis, August 2007 to September, 2009

The investors in various markets feared that some of the assets had suddenly become worth much less than they had thought and the loss of confidence that comes when they realized that there are hidden losses among their assets was the collapse of confidence. The second type of loss of confidence is related to action that investors and institutions take when they realized they no longer trust the proxy signs in the economy, it represented withdrawal of confidence.

Both types of confidence were part of event after Lehman bankruptcy which involved the fall of A.I.G and sudden demand by Bernanke for $700 billion to handle the crisis. Bernanke felt that if A.I.G went bankrupt this might break financial system and a decision to invest $80 billion in A.I.G. While the decision by the Fed to back A.I.G may have eliminated the breakdown in financial system, it also led to some confusion that why the FED had let Lehman fail? This was an economic 9/11!!